Washington Property Tax Records

Washington property tax records are public documents kept by county assessors and treasurers across all 39 counties in the state. Each county assessor sets the assessed value for every taxable parcel, and the county treasurer handles billing and collection. You can search Washington property tax records online through individual county portals, which let you look up ownership details, assessed values, tax history, and payment status by parcel number, owner name, or property address. The Washington State Department of Revenue oversees property tax administration statewide and provides resources for property owners and researchers seeking access to these records.

Washington Property Tax Records Overview

Where to Find Washington Property Tax Records

Property tax records in Washington are kept at the county level. The county assessor holds assessment data including ownership details, parcel maps, and valuation history. The county treasurer holds billing and payment records. Both offices are public, and most records must be open for inspection during regular office hours under RCW 84.40.020. Confidential income data submitted for exemption applications is exempt from public disclosure under RCW 42.56.070.

Many counties offer free online property search tools. Most let you look up a parcel by address, owner name, or parcel number. Results typically show current and prior assessed values, land value, improvement value, tax amounts, payment history, and sales records. Some portals include a GIS map view showing parcel boundaries on aerial imagery. If you are unsure which county portal to use, the Washington State Department of Revenue maintains a county contacts directory with direct links to each county's assessor and treasurer websites.

The Washington State Digital Archives holds historical property tax records going back to the 19th century for many counties. Digitized collections include field books, photographic record cards, assessment rolls, and deed records. These are useful for researching older properties or tracing ownership history over many decades. Records from the Assessor's office typically show assessed values, building characteristics, and parcel boundaries at the time of each inspection cycle.

The Washington State Department of Revenue property tax portal publishes guidance on assessment methods, taxpayer rights, levy calculations, and exemption programs across all 39 counties. The DOR does not collect property taxes. It supervises the system, conducts annual ratio studies, and performs administrative reviews of county assessor offices to check for compliance with state law.

The DOR's personal property tax section explains how business equipment, machinery, and other non-real-property assets are assessed at the county level each year.

The main DOR property tax portal is where most statewide questions on assessment, collection, and tax relief start. It links to all major programs and county contacts.

The Washington State Department of Revenue operates this property tax portal, which serves as the statewide hub for guidance on assessment methods, tax relief programs, and county administration requirements.

How to Search Property Tax Records in Washington

Searching Washington property tax records usually starts with the county assessor's online tool for the county where the property sits. Many counties use vendor-hosted platforms. Common systems include TaxSifter (TerraScan), PropertyAccess (PACS by N. Harris Computer Corporation), TrueAutomation, MapGeo, and COMPAS. Others have custom portals. All of them let you search by parcel number, owner name, or street address.

A typical county search result shows: current and prior year assessed values broken into land and improvement components, ownership and mailing address, tax code area, sales history with transaction dates and prices, and a payment status summary. Many portals also link directly to an online payment option and a GIS map view. The GIS map overlays parcel boundaries on aerial photography and shows nearby parcels, roads, zoning, and district boundaries. It is important to note that these map displays show assessor tax parcel boundaries, not legal property lines. Only a licensed survey establishes legal boundaries.

For in-person access, state law under RCW 84.40.020 requires the assessor's office to make property listings and supporting documents available during regular office hours. Staff can help you search by parcel number, owner name, or address. You can also request copies of assessment records, appraisal notes, and parcel maps. Copy fees vary by county. Certified copies of recorded deeds and other land documents are handled by the county auditor's office, not the assessor.

The county auditor, acting as county recorder, keeps deeds, mortgages, liens, plats, and easements. Many counties provide online document search tools through their auditor's office. These let you search by grantor or grantee name, document type, recording date, or parcel number. Most recorded documents from the 1970s forward are available online through county or state portals.

The DOR's personal property tax page covers how business equipment and movable assets are valued and taxed at the county level, including reporting deadlines and exemption rules for household goods and certain business assets.

Washington Property Tax Assessment Process

Washington law requires all real and personal property to be assessed at 100 percent of true and fair market value. True and fair market value is defined as the price a willing buyer would pay a willing seller when neither is under pressure to complete the transaction. The county assessor is responsible for setting this value each year. Physical inspection of each property must happen at least once every six years under state rules, though many counties now inspect on shorter cycles.

The assessment roll is the official record of all taxable parcels in a county. It lists owner name, mailing address, legal description, parcel number, and assessed value as of January 1. Under RCW 84.40, assessors must maintain and make this roll available to the public. Real property includes land, improvements on the land, and fixtures permanently attached to structures. Personal property covers business machinery, equipment, furniture, and supplies. Household goods kept only for personal use are exempt from personal property tax.

Assessors use three professional appraisal methods: the sales comparison approach (comparing recent similar sales), the cost approach (estimating replacement cost minus depreciation), and the income approach (for commercial income-producing properties). Each year, the DOR conducts ratio studies to verify that county assessors are applying market value consistently. These studies compare assessed values to actual sale prices and flag counties where assessments are significantly above or below market.

The DOR's ratio study program runs annual checks in all 39 counties to confirm that property assessments reflect real market conditions. Results are public and help taxpayers understand how their county compares to the statewide standard.

Property Tax Payment Schedule and Deadlines

Washington property taxes are paid in two installments each year. The first half is due on or before April 30. The second half is due on or before October 31. If the total tax owed is $50 or less, the full year must be paid by April 30. County treasurers mail tax statements by March 15 of each year as required under RCW 84.56. Not receiving a statement does not waive the payment obligation.

When taxes are not paid on time, interest and penalties apply. After April 30, taxes are considered delinquent and accrue 1 percent interest per month. A 3 percent penalty is added on June 1. If taxes remain unpaid through December 1, an additional 8 percent penalty applies. For residential parcels with four or fewer units, some counties apply a reduced interest rate of 0.75 percent per month with modified penalty timing depending on the assessment year. Contact your county treasurer for the exact schedule that applies to your parcel.

Most counties now accept online payments via eCheck, credit card, or debit card. Convenience fees apply to card payments. Many offer payment by phone, drop box, mail, or in person. Mailed checks must be postmarked by the due date to count as timely. If real property taxes go unpaid for three or more years, the county treasurer begins foreclosure proceedings under RCW 84.64.

Property Tax Exemptions and Tax Relief in Washington

Washington offers several programs that reduce or defer property taxes for eligible property owners. The most widely used is the senior citizen and disabled persons exemption. To qualify, you must be at least 61 years old or retired due to disability, and your combined disposable income must fall below the qualifying threshold for your county. Income limits vary by county and have increased in recent years. The exemption reduces your tax bill based on your income and the assessed value of your home. Applications go through the county assessor's office.

The Washington DOR exemptions and deferrals page covers all available programs. These include the senior and disabled persons deferral, which lets qualifying homeowners defer payment to a lien against the property that accrues 5 percent simple interest until the home is sold or transferred. There is also a limited income deferral for homeowners who need to postpone the second half installment. A veterans widow or widower assistance grant provides direct payment help to surviving spouses of qualifying veterans who died from service-connected conditions. Each program has its own income limits and eligibility rules.

Nonprofit organizations can apply for property tax abatement if they own and exclusively use property for exempt activities defined by state law. Applications go to the DOR, not the county. Annual renewals are due by March 31. The DOR's nonprofit exemptions page walks through the registration process, renewal steps, and delegation options for organizations with multiple locations.

Current use programs are available for agricultural, forest, and open space land. These programs allow certain qualifying properties to be assessed based on their current use rather than market value, which can significantly reduce tax obligations for farming and forestry operations.

This DOR page outlines each exemption and deferral program in Washington, with eligibility requirements and links to application forms for senior citizens, disabled persons, veterans, and qualifying nonprofit organizations.

Appealing Washington Property Tax Assessments

If you disagree with your property's assessed value, you can appeal. Washington law presumes that the assessor's value is correct. To overturn it, you must present clear and convincing evidence that the assessor made a mistake. The first step is filing a petition with the County Board of Equalization (BOE). You typically have 30 to 60 days from the mailing date of your Change of Value Notice to file, depending on the county. The BOE schedules a hearing, reviews your evidence, and issues an order.

If the BOE upholds the assessor's value and you still disagree, you can appeal to the Washington State Board of Tax Appeals (BTA). The BTA is the only independent state-level administrative forum for tax disputes in Washington. It is located at 1110 Capitol Way S, Suite 307, Olympia, WA 98504. The BTA also hears direct appeals, where the taxpayer, assessor, and county board all agree to bypass the BOE and go straight to the state level under RCW 84.40.038. You must file your BTA appeal within 30 days of the BOE's mailing date. The BTA offers both informal and formal hearing processes. Formal decisions can be further appealed to Superior Court, but all taxes must be paid before court review.

The Washington State Board of Tax Appeals is the independent state-level forum where property owners can challenge county Board of Equalization decisions on assessed values, exemption denials, and other property tax disputes.

Washington Personal Property Tax Records

Personal property tax applies to business equipment, machinery, furniture, fixtures, and supplies used in operating a business in Washington. Business owners must report their personal property to the county assessor annually by April 30. The assessor values personal property at 100 percent of market value using depreciation schedules approved by the DOR. The taxed amount is then added to the property's tax bill just like real property taxes, with the same April 30 and October 31 due dates.

One important exemption applies to heads of household. Each qualifying head of household may exempt up to $15,000 of actual value from personal property tax under state law. Mobile homes occupy a unique category: they are generally classified as real property for tax purposes once permanently installed on a foundation with fixed utility connections, but they may be treated differently for collection purposes when being moved. See RCW 84.04.090 for the statutory definition.

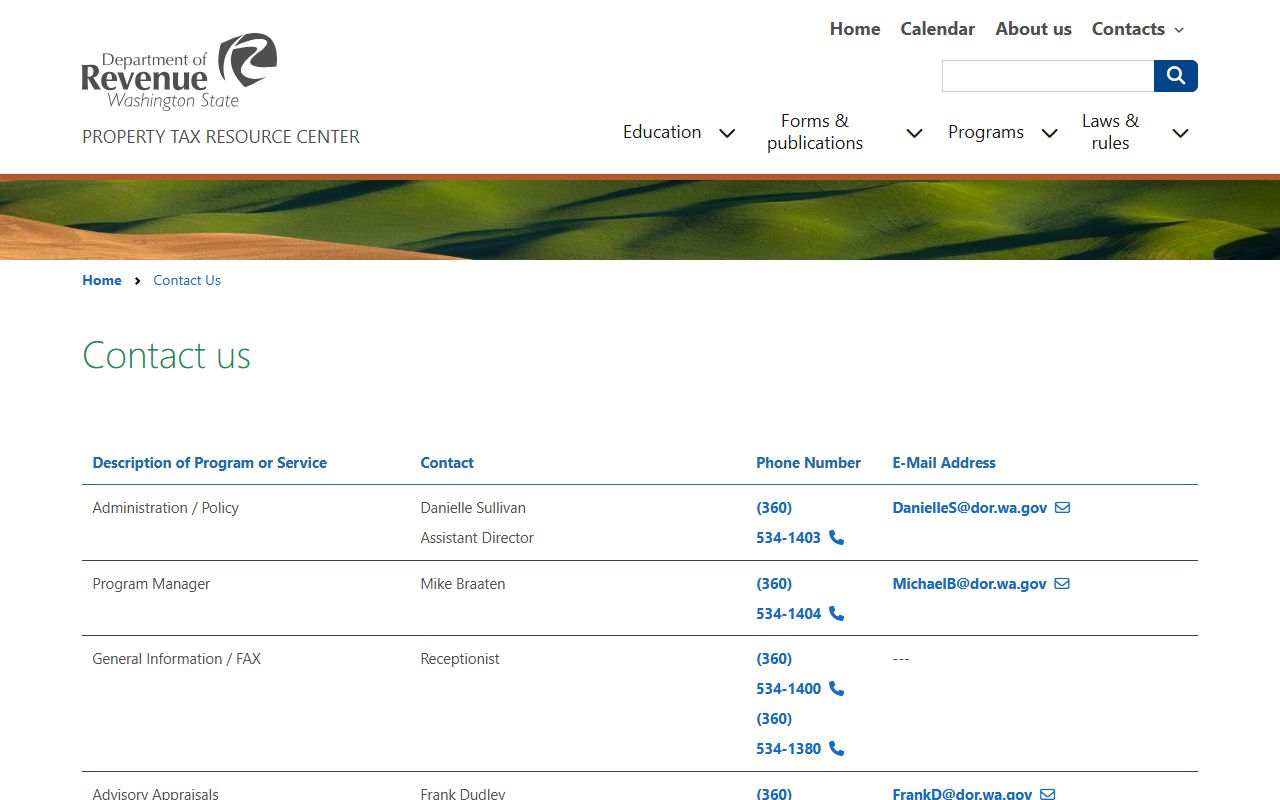

The DOR Property Tax Division contact page lists direct phone numbers and email addresses for each program specialist, including contacts for personal property, senior exemptions, levy calculations, and ratio studies across Washington State.

Historical Washington Property Tax Records

Property tax was the first tax levied in Washington and continues to be one of the most important revenue sources for schools, fire protection, libraries, and parks. Today it accounts for roughly 30 percent of all state and local tax revenue. Historical property tax records go back to the territorial period for many counties. The Washington State Digital Archives holds digitized field books, photographic record cards, assessment rolls, and deed records for dozens of counties.

Older records are often organized by addition, block, and lot rather than by parcel number. Searching may require the legal description of the property. For records predating digital archives, county assessor offices may hold physical files or microfilm. The Washington State Archives maintains regional branch offices with historical county records available for in-person research.

The Washington State Board of Tax Appeals maintains records of historical valuation decisions that can provide useful reference material for understanding how specific property types have been assessed and challenged in Washington over time.

Browse Washington Property Tax Records by County

Washington has 39 counties, each with its own assessor and treasurer who maintain property tax records for parcels in that jurisdiction. Select a county to find local search tools, office addresses, payment options, and exemption program details.

Washington Property Tax Records by City

Property tax records are filed and managed at the county level, not the city level. Knowing your city helps identify the right county assessor and treasurer. Below are major Washington cities with property tax record pages covering local offices, search tools, and tax resources.